Last week Plasma went live with the public beta for their highly anticipated neobanking product, Plasma One.

The numbers are hard to ignore: Plasma One is already powering over $400K in daily card spend. Demand for the Platinum card, which offers 4% base cashback and as much as 10% on AI spend and flights, has pushed users to lock more than $3.2 million in XPL within days of launch.

By nearly every meaningful metric, Plasma One is shaping up to be one of the strongest neobank launches we've seen. In this report, we dig into what's driving this and the numbers behind it.

What Is Plasma One?

Plasma One is a globally accessible, stablecoin-powered dollar account with a Visa card that returns 2-4% cashback on every purchase, and as much as 10% on selected categories like AI spend and flights.

When building Plasma One, founder Paul Faecks says they rethought "what the modern banking experience should look like in an internet-native world." To us, this means a single place to store, save, and spend money with ultra-competitive terms and a beautiful user experience.

Aside from its flagship dollar account, Plasma One also offers USD, EUR, GBP, and MXN banking rails, and a ~4% APR Earn vault powered by @aave stablecoin lending markets on the Plasma blockchain.

Plasma One's Launch in Numbers

Plasma One initially launched in mid-March with an invite-gated private beta that offered 3% cashback on all spend for all users.

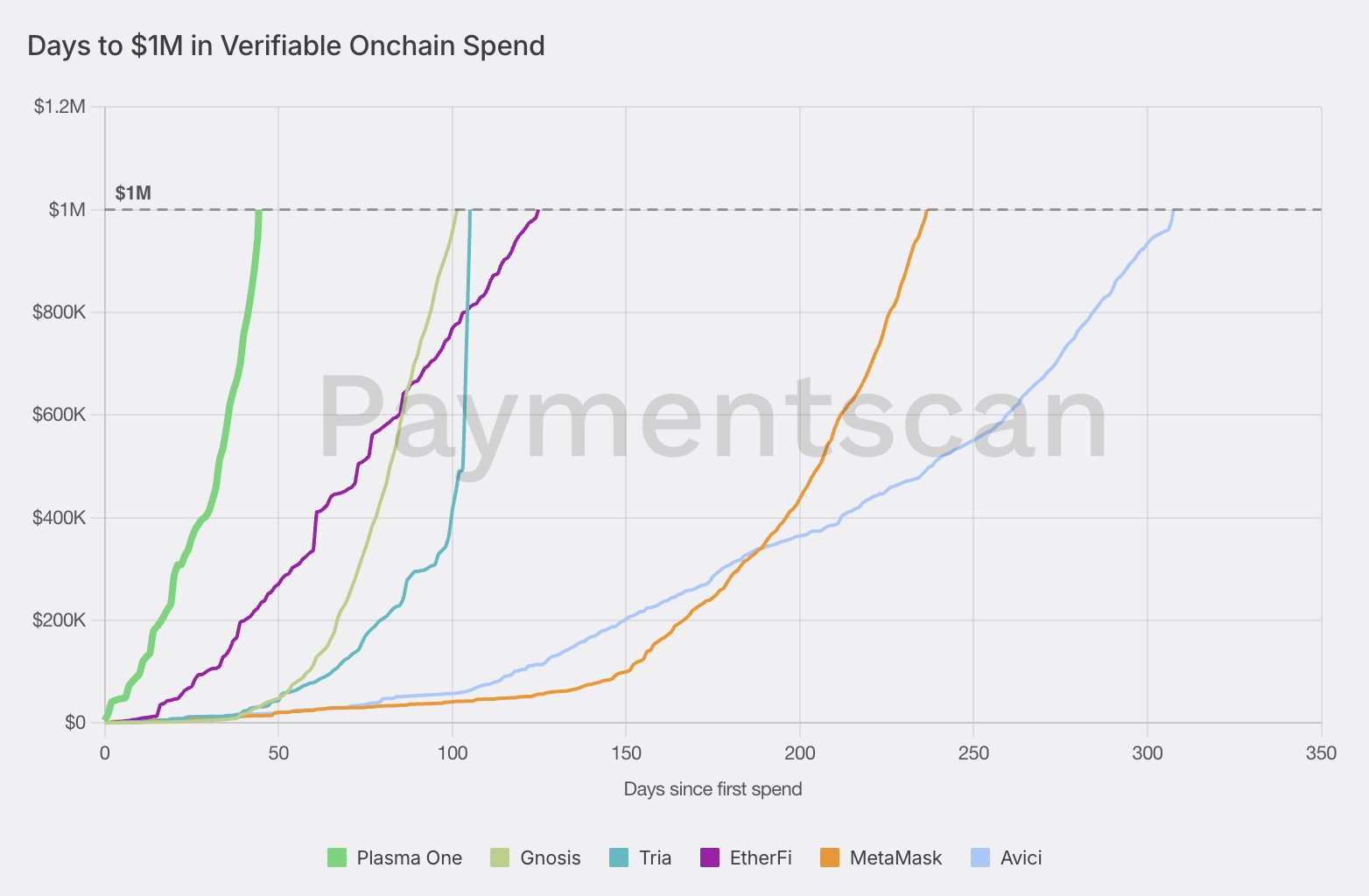

This alone was enough for users to flock over and try it: in just 45 days, Plasma One hit $1M in verifiable onchain card spend, making it the fastest stablecoin card ever to do so.

Number of days to reach $1M in verifiable spend. Cards for which only deposit flows can be tracked are excluded. Plasma One data is counted from private beta launch (March 17th).

Now, a little more than 45 days later, Plasma One is live in public beta and has grown a further 10X, surpassing:

- $10M in verifiable card spend

- 34,000 registered users

- 7,700 active card users

Plasma One hit these numbers with iOS users alone; Android support is set to release in the coming weeks.

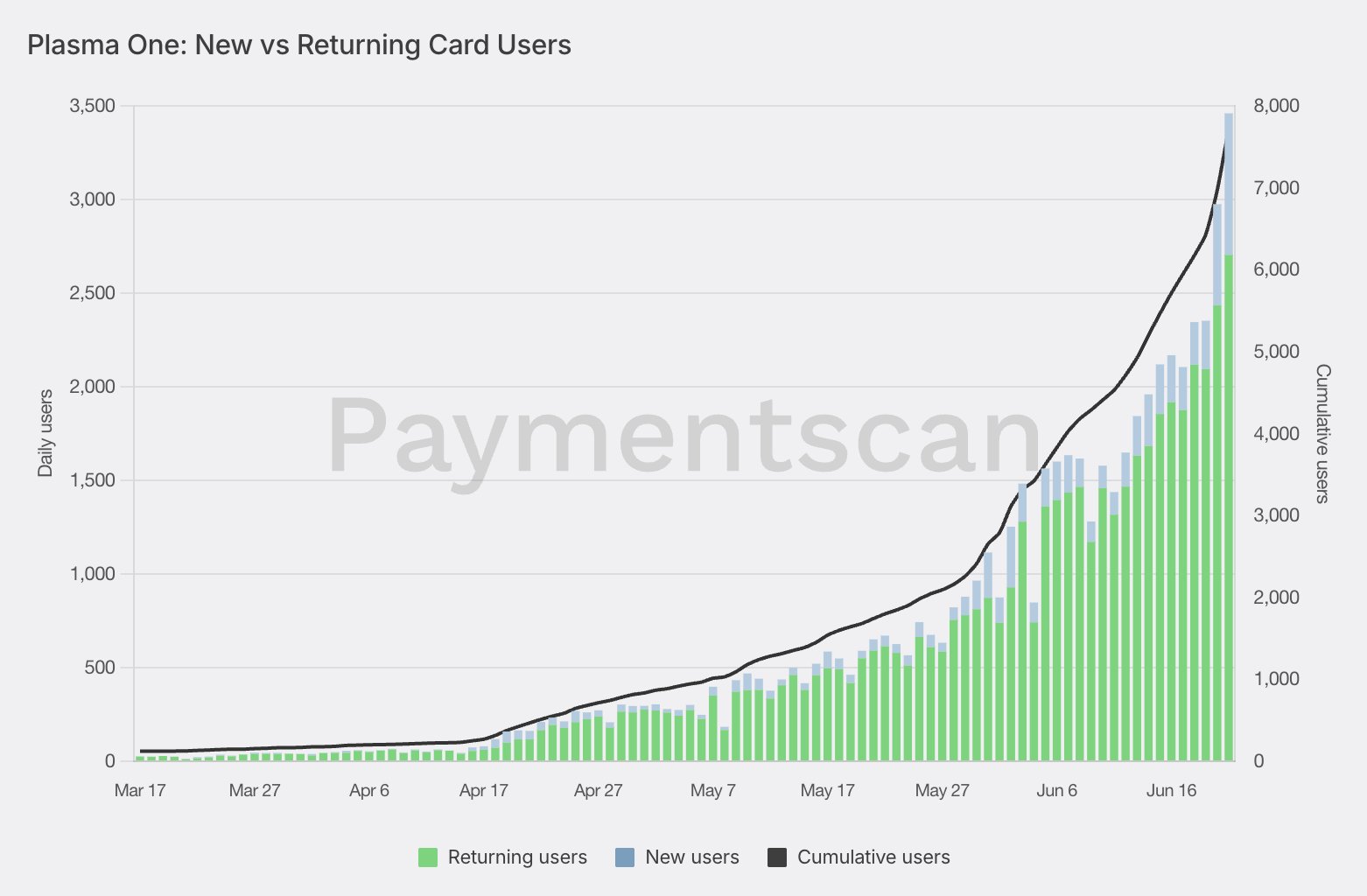

Digging deeper into user activity shows that, from day to day, over 90% of Plasma One card users return to spend again:

Plasma One returning, new, and cumulative card users by day. Card users are defined as addresses that made at least one card payment on that day.

Given this stickiness, we anticipate card spend will increase significantly in the coming weeks as new users who initially deposited small amounts begin to make more substantial deposits.

Plasma One Tiers and the XPL Token Sink

As part of last week's public launch, Plasma unveiled three tiers for their card: a Lite tier accessible to anyone, as well as more exclusive Core and Platinum tiers which create a sink for Plasma's governance token, XPL.

The Lite tier offers one free Visa Signature card with 2% cashback on all spend. This is Plasma's answer to incumbent stablecoin card programs which charge a fee for card issuance and return lower cashback, and yet still see huge demand globally.

The next tier is Core, available for a $120 annual fee or by locking 20K XPL for 12 months. As part of the public launch, users who sign up before Wednesday receive one year of Core membership at no cost.

With a total of over $1,000 in annual value, Core brings:

- Lower fees e.g. FX

- 3% base cashback

- 5% cashback on AI spend

- Free ChatGPT Go subscription

- 1% referral rewards

This tier makes it clear that Plasma One is not only looking to own the pool of crypto-native users, but also the far larger (and far more rapidly expanding) pool of internet-native AI users.

(Microsoft estimates that over 16% of the global population uses AI, while data from 2024 suggests crypto ownership is less than half as frequent, not to mention the cyclical nature of the industry).

The card tier that has stirred up the most interest is the highly exclusive Platinum tier: a Visa Infinite card boasting over $10,000 in annual value, including:

- 4% cashback

- 10% cashback on AI spend

- Claude Pro and ChatGPT Plus

- Up to $600 of airline credit with eligible airlines

- 1% referral rewards

Platinum is exclusive to XPL holders, requiring a 150K XPL stake for 12 months. For the first 30 days post-launch, this has been reduced to 100K XPL.

Per onchain data, demand for this tier has been substantial: since launch, over 350 users have upgraded to Platinum, locking some $3.2M in XPL in under 7 days.

This means that 1 in every 3 wallets holding over 100K XPL has upgraded to Platinum, which corresponds to over 1% of XPL's circulating supply that has now been removed from the market.

Plasma is the Settlement Layer

Cashback and other features aside, Plasma One stands out amongst other stablecoin neobanks for one simple reason: Plasma also owns the settlement layer. The Plasma blockchain is purpose-built for payments, with fast consensus, low fees, and deep stablecoin liquidity.

All of the data in this report is derived from Plasma One's onchain architecture. Users' funds are held in USDT, Tether's leading stablecoin, in self-custodial wallets. Only when a card is tapped or swiped is collateral locked onchain, with clearing taking place once daily for sub-$0.01 fees.

It should come as no surprise that Plasma One isn't the only card product settling on the Plasma blockchain. In May, $1.6B social commerce platform Whop unveiled a card for its creators, which utilizes Plasma for settlement.

While Whop's card settlement addresses are not public, our analysis of payment flows on Plasma suggests a further $8M in card payments have been settled on the chain since the beginning of May, with cumulative payment volume following an exponential trajectory:

Cumulative card payment volume settled on Plasma.

The Takeaway

Plasma One's public beta provides one of the clearest early examples of demand for a stablecoin-native banking product. In just a few months, it has accumulated more than $10M in card spend, attracted tens of thousands of users, and generated meaningful demand for XPL through its tiers. Looking ahead, we'll be watching Plasma One closely to see if it can break out and attract a new, non-crypto user base.

For more data-driven insights into crypto payments and stablecoin adoption, follow us on X.